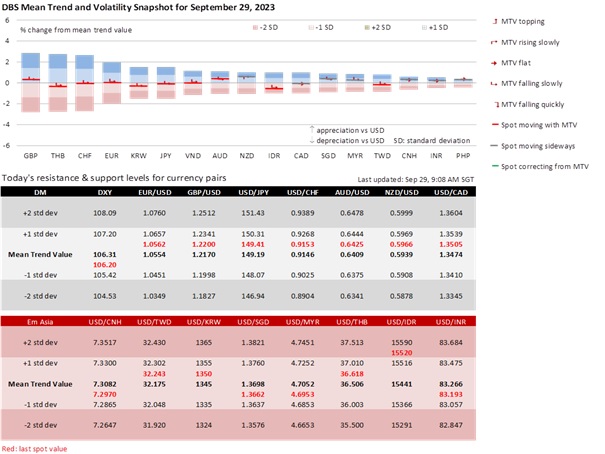

DXY appreciated another 2.4% to 106.1 this month, on top of August’s 1.7% rally after an aggressive sell-off in early July. The DXY’s recovery gained traction after the Fed stopped projecting a US recession at its FOMC meeting on 26 July, followed by two months of stronger inflation readings. Today’s PCE deflator inflation should rise like the CPI a fortnight ago. Although the Fed paused on 20 September, it convinced markets of its “higher for longer rates” bias by keeping the door open for an additional hike later this year and projecting fewer cuts in 2024. The US Treasury 10Y yield farther above 4% to 4.57% in September. While markets agreed with the Fed’s soft-landing outlook, they feared more rate hikes would increase recession risks in Europe.

Three European currencies in the DXY basket depreciated most in September, led by the CHF (-4%), the GBP (3.5%), and the EUR (2.9%). The European Central Bank’s surprise rate hike on 14 September could not eclipse the Eurozone economy’s deteriorating outlook flagged by the ECB in July. Five economic institutes predicted that the German recession would be worse than initially thought. Germany’s CPI inflation dove to a preliminary 4.5% YoY in September from 6.1% in August, its lowest reading since February 2022. Today, consensus expects a similar plunge in the Eurozone’s CPI estimate to 4.5% from 4.2%. Not surprisingly, ECB officials have been signalling a pause at the next governing council meeting on 26 October, with the narrative shifting to keeping rates “high for longer.” EUR/USD peaked at 1.1276 around mid-July and plunged to a ten-month low of 1.0488 in late September.

USD/CHF bottomed at 0.8553 and surged to 0.9225, while GBP/USD spiralled from 1.3142 to 1.2111 this quarter. USD/CHF and GBP/USD are back inside the 0.90-0.94 and 1.18-1.2450 ranges of December-March. Markets expected the Swiss National Bank and the Bank of England to hike on 21 September, but they paused instead on declining inflation and growth worries. Unlike the US, the UK’s CPI and core inflation did not rise and fell instead. This quarter, Switzerland’s headline and core inflation returned to the 0-2% target. GDP growth flattened to 0% QoQ sa in 2Q23 from 0.3% the previous quarter in Switzerland and to -0.5% MoM in July from 0.2% in 2Q23 in the UK.

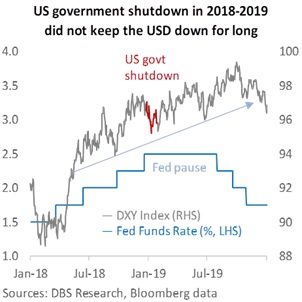

In the immediate term, markets are bracing for a possible US government shutdown in the first fortnight of October. According to the New York Times, statisticians have collected the data for the September jobs report, but a prolonged shutdown could affect the next survey to be conducted in mid-October. The Fed could also lose information about CPI inflation (scheduled for 12 October) before its FOMC decision on 1 November. However, the Fed is unaffected by the shutdown, with many Fed officials speaking in the first half of October. Earlier this week, we highlighted some observations from the last shutdown between December 2018 and January 2019. DXY gave back gains only after the shutdown began but regained its composure when a resolution was in sight in Congress. All said, we remain mindful that the DXY’s outlook has been driven as much by the weakness in Europe as the Fed’s optimism for a soft landing.

Quote of the day

“The greatest failure of all is the failure to act when action is needed.”

John Wooden

29 September in history

In 2008, the stock market crashed after the first vote in the US House of Representatives on the Emergency Economic Stabilization Act failed, leading to the Great Recession.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.