Related Insights

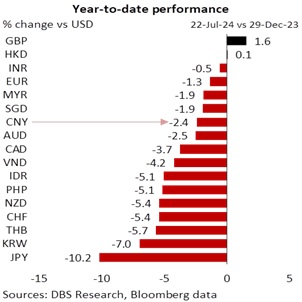

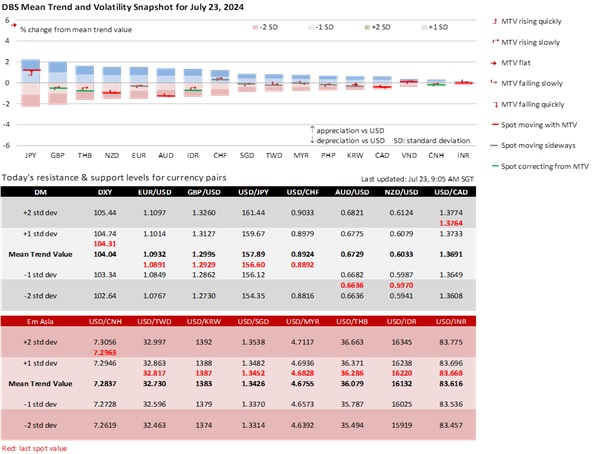

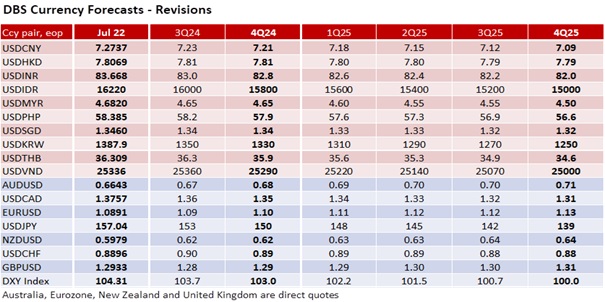

The CNY depreciated by 0.1% to 7.2738 per USD after the People’s Bank of China surprised with a 10bps cut in the 7-day repo rate to 1.70%. The central bank also lowered the 1Y and 5Y loan prime rates by the same quantum to 3.35% and 23.85%, respectively, one week after China’s GDP growth slowed to 4.7% YoY in 2Q24 from 5.3% in 1Q24. Despite the worries over China’s economy, property sector, and local government debt, the CNY’s 2.4% YTD depreciation this year was muted compared to the 7% and 10.2% declines in the KRW and JPY, respectively. Despite its steady rise this year, USD/CNY has yet to break out of the 7.10-7.35 range set in June 2023. We have not forgotten USD/CNY’s fall from 7.30 to 7.10 on aggressive Fed cut bets last November-December. The futures market is betting that this Friday’s US PCE deflators will provide the Fed the confidence to deliver 2-3 rate cuts in September-December. We believe USD/CNY will fall to 7.21 by the end of this year on the two Fed cuts we expect later this year.

AUD/USD peaked at 0.68 on July 11 and fell to 0.6643 on Monday, back inside the 0.6575-0.6700 range seen between mid-May and early July. Apart from China’s uninspiring economy, AUD has been under pressure alongside commodities over the past week due to uncertainties over the US Presidential elections. For example, copper fell 17% from the year’s high of USD505/lb.70 (May 21) to 420 on Monday. However, US equities rallied in the overnight market after US President Joe Biden ended his re-election bid with Democrats uniting behind Vice President Kamala Harris as the party’s nomination to take on Donald Trump at the elections. A less one-sided race to the White House coupled with Fed cuts could weaken the USD and support the AUD later in the coming months.

NZD/USD depreciated by 0.5% to 0.5980 on Monday, its weakest level since May 2. The kiwi has been under pressure after the Reserve Bank of New Zealand’s dovish tilt at its meeting on July 11. The OIS market sees the RBNZ lowering its official cash rate at the remaining three meetings (August 14, October 9, and November 27) this year by a total 75 bps to 4.75%. New Zealand’s CPI inflation is set to return to its 1-3% target band in 3Q24. Headline inflation fell from 4.0% YoY in 1Q24 to 3.3% YoY in 2Q24, its lowest level since 2Q21. Tradeable inflation contracted a third quarter by 0.5% QoQ in 2Q24 vs. 0.7% in the previous quarter. NZD/USD has given back 65% of its rise from 0.5850 (this year’s weakest level on April 19) to 0.6220 (the year’s highest level on June 12). The next support level is around the 75% Fibonacci retracement level of 0.5945, followed by a trendline support level near 0.59, just above this year’s weakest level of 0.5850.

Quote of the day

”Live as if you were to die tomorrow. Learn as if you were to live forever.”

Mahatma Gandhi

23 July in history

The Ford Motor Company sold its first car in 1903.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.