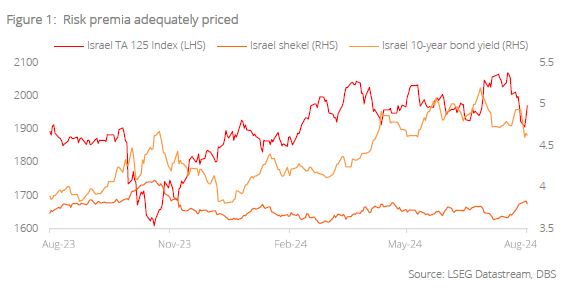

- Current risk premium appears to be on the same level as those seen during the onset of the Israel-Hamas conflict in Oct 2023

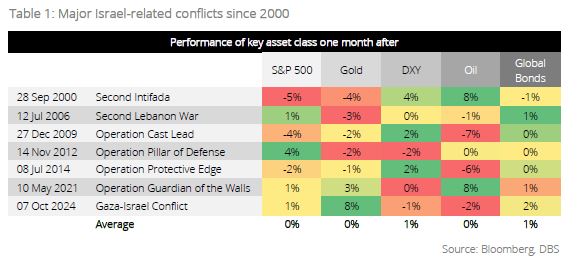

- Historically, Middle East conflicts have muted impact on the markets with gold and oil serving as effective hedges

- Conflict still spells upside potential for oil, though magnitude of impact might be muted due to growing US dominance in crude production

- Geopolitical risk just one of many tailwinds for safe haven gold; risk-off episodes will boost safe haven demand

- Stay anchored in our CIO Barbell Strategy amid ongoing geopolitical tensions as this strategy allows clients to capture long-term opportunities while generating stable income to mitigate short-term market volatility

Related Insights

- Cloudy Outlook Ahead30 Aug 2024

- FX Tactical Ideas: Long AUD-NZD at Bottom of Ascending Channel30 Aug 2024

- CDL Hospitality Trusts30 Aug 2024

The Japanese yen remains a central focus for carry trade unwinds; But rising Middle East tension also warrants close attention. While predicting developments on the ground is difficult, an all-out war seems to have been averted for now, with nations urging for de-escalation and diplomatic solutions.

Risk premium on par with Oct 2023’s high. Amid heightened geopolitical risks, we assessed risk premiums relative to Oct 2023 by examining Israel’s local markets. Israel’s 10-year bond yields peaked at 4.7% last October before returning to pre-conflict levels of 3.8%. Reflecting recent tensions, bond yields have risen again, reaching a peak of 5.2% and currently hovering near the October high of 4.6%. Our analysis shows that risk premiums are now comparable with those seen at the peak in Oct 2023, the onset of the Israel-Hamas conflict.

In contrast, Israel’s currency and equity markets have demonstrated more stability. The Israeli shekel and the Tel Aviv 125 stock market index have fully recovered from their October lows and are now approaching pre-conflict levels. Overall, investors seem cautiously optimistic, anticipating that the current tensions will eventually ease.

Historically, conflicts in the Middle East have limited impact on financial markets. Investors appear accustomed to such situations. Our analysis from when the Hamas-Israel conflict first erupted in October last year, revealed that beyond immediate headlines and reactions, Middle East conflicts have historically had a muted impact on financial markets. The most effective hedges against further escalation remain to be gold and oil.

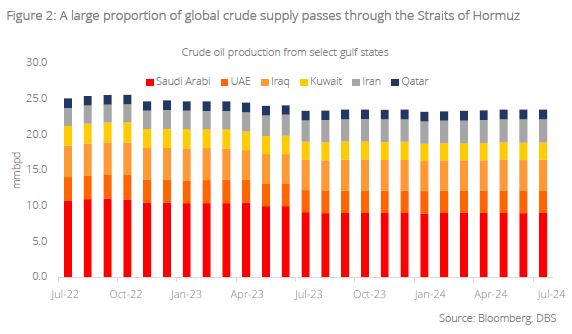

Middle East tensions spell upside potential for oil. The impact of Middle East conflicts on global financial markets have traditionally been through oil prices. This is unsurprising as approximately a quarter of global crude production comes from the region, and a third of its related trade passes through the Straits of Hormuz; any disruptions to production and trade as a result of geopolitical conflict will materially impact global supply and raise prices. We saw this happen late last year on the back of attacks on ships in the Red Sea from Nov 2023 to Jan 2024, causing a c.5.5% increase in oil prices during the same period.

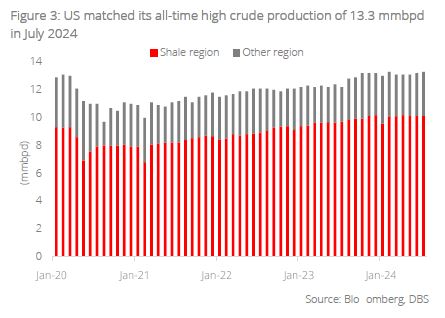

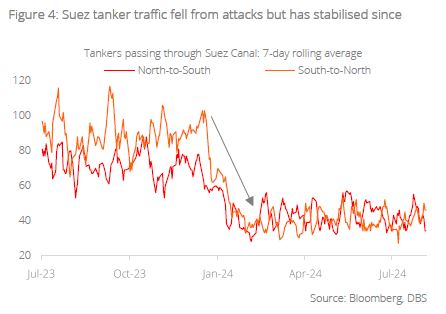

Impact will still be there, but possibly more muted. We believe this time is no different: an escalation in conflict between Iran and Israel presents upside potential for oil prices. However, the magnitude of the upside may not be as significant as some expect. This is due to two reasons: i) while the Middle East remains a key crude producer, the US has increased its production over time through its burgeoning shale supply, and this has reduced the former’s influence as a swing producer; ii) global supply chains have likely adjusted to the drop in tanker traffic in the Suez Canal by now. On point (ii), unless the escalation in conflict is severe enough to further reduce tanker traffic, we will likely not see significant oil price upside from trade disruptions specifically.

Safe haven gold a potential beneficiary. Gold has not had a shortage of tailwinds in recent times. Decelerating growth, easing inflation, and a softening labour market in the US are setting the stage for Fed rate cuts later in the year, and laying the foundation for further rallies for non-interest-bearing gold. Furthermore, central bank gold buying remains robust, driven by the threat of monetary debasement, fiscal sustainability concerns, and de-dollarisation. The US elections in November also present potential right-tail risk for the precious metal. Heightened geopolitical tensions add to that mix, giving gold yet more room for upside. Should the conflict between Iran and Israel escalate into all-out war, we believe gold will likely experience a short-term boost through elevated safe haven demand.

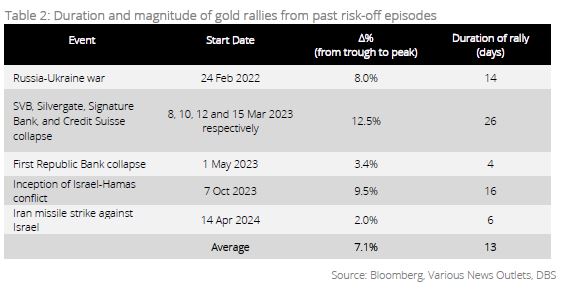

How much of a boost will bullion receive? Based on historical analysis of recent risk-off incidents, we found that gold rallies after such episodes lasted 13 days on average and resulted in an average price increase of 7.1% trough to peak. It is reasonable to assume that a war between Iran and Israel will likely result in a rally of similar length and magnitude. However, the exact impact will really depend on how the conflict plays out; should the conflict be contained between the two nations, the resultant rally will be a likely be a one-off event. However, if the conflict results in wider regional instability, we could see multiple gold rallies with each episode of escalation.

Stay with Barbell Strategy in uncertain times. Since the onset of the Israel-Hamas war in Oct 2023, our DBS CIO Barbell Strategy has demonstrated resilience, delivering a stellar return of 15.6% which outperformed the 14.8% return of the 50-50 composite of global equities and bonds index. As geopolitical tensions persist, we continue to advocate adopting our Barbell Strategy to build a robust investment portfolio during such challenging times. On the growth side, invest in companies that are well positioned to capture long-term secular trends and benefit as the world transits to a digital economy. On the income side, invest in dividend yielding equities such as REITs and bonds. The income nature of these assets will provide resilience to the overall portfolio. In addition, risk diversifiers such as gold, which have low correlations to equities and bonds, can further reduce portfolio volatility and drawdowns.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Cloudy Outlook Ahead30 Aug 2024

- FX Tactical Ideas: Long AUD-NZD at Bottom of Ascending Channel30 Aug 2024

- CDL Hospitality Trusts30 Aug 2024

Related Insights

- Cloudy Outlook Ahead30 Aug 2024

- FX Tactical Ideas: Long AUD-NZD at Bottom of Ascending Channel30 Aug 2024

- CDL Hospitality Trusts30 Aug 2024