- Equities: Global equities rebound strongly after early Aug sell-off, driven by positive economic data and rate cut optimum

- Credit: As rate tightening cycle nears its end, investors can clip the higher coupons in IG credit on lower volatility as rates and spreads are no longer highly correlated

- FX: USD/JPY eyeing lower levels after its short covering from 141.70 on 5 Aug; USD/THB has the scope to fall further to 34 on a weaker USD

- Rates: Panic in USD rates receded; no longer makes sense for the market to factor in aggressive Fed easing

- The Week Ahead: Keep a lookout for US Change in Initial Jobless Claims; Japan CPI

相關見解

- 人民幣雙向波動27 Aug 2024

- 每周外匯速遞 - 美元續跌 警惕回調風險26 Aug 2024

- Economics Weekly: Continued Moderation16 Aug 2024

Stocks continue recovery amid optimism. Following the early August sell-off, stocks rebounded strongly with Nasdaq leading the recovery, up 5.3% for the week, followed by the S&P 500, up 3.9%. This was supported by positive retail sales and cooling inflation data, its lowest reading in more than three years. However, the housing sector showed signs of strain with building permits and housing starts dropping to their lowest levels since the early pandemic.

European markets rallied alongside the US, buoyed by expansion of the Eurozone economy, +0.3% in 2Q. The Euro STOXX 50 and Dax were up 3.5% and 3.4% for the week. Over in Japan, the Nikkei 225 was up 8.7%, supported by a weaker yen and stronger than expected US economic data. China, on the other hand, saw modest gains despite posting weaker-than-expected industrial production numbers and continued declines in new home prices. The SHCOMP and Hang Seng were up 0.6% and 2.0% for the week.

Topic in focus: Tactical play on small caps as Fed policy eases. On Wednesday (14 Aug 2024), July’s CPI numbers came in lower than expected (2.9% y/y vs consensus 3.0% y/y), and it marks the first time since Mar 2021 that CPI has fallen below 3%. This strengthens the case for initiating a rate cut cycle in September which will likely benefit small caps. Medium-term momentum for the small caps space include:

- Rate cuts and lower borrowing cost to buoy small caps earnings: Small caps companies have a larger proportion of debt maturing within five years as compared to larger companies (c.67% for S&P 600 Small Cap vs c.45% for S&P 500). As the Fed embarks on monetary easing, small cap companies will be able to refinance at lower rates, reduce their borrowing cost, and boost earnings.

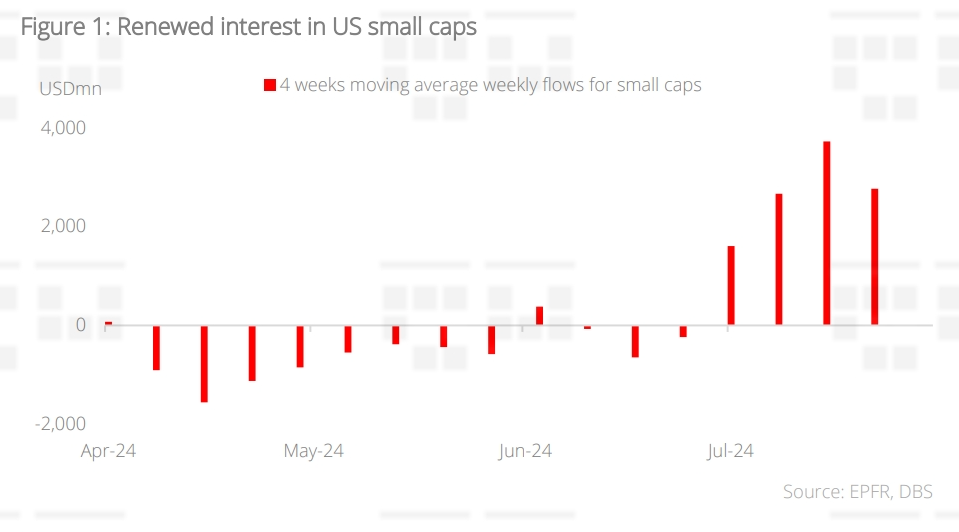

- Fund flows suggest renewed interest in US small caps as rate cuts loom: In the three months before June's CPI data release, small cap equity funds saw weekly outflows. Since the release of June’s data (which fuelled expectations of a September cut), small cap equity funds attracted a combined inflows of USD11bn in four weeks (ending 7 Aug).

- Attractive “broadening rally” play amid steep valuation discount: At 17.7x, the S&P 600 Small Cap index’s forward P/E is currently well below its 20-year average. Above all, the index is also trading at a 22.9% discount to the S&P 500.

本資訊是由星展銀行集團公司(公司註冊號: 196800306E)(以下簡稱“星展銀行”)發佈僅供參考。其所依據的資訊或意見搜集自據信可靠之來源,但未經星展銀行、其關係企業、關聯公司及聯屬公司(統稱“星展集團”獨立核實,在法律允許的最大範圍內,星展集團針對本資訊的準確性、完整性、時效性或者正確性不作任何聲明或保證(含明示或暗示)。本資訊所含的意見和預期內容可能隨時更改,恕不另行通知。本資訊的發佈和散佈不構成也不意味著星展集團對資訊中出現的任何個人、實體、服務或產品表示任何形式的認可。以往的任何業績、推斷、預測或結果模擬並不必然代表任何投資或證券的未來或可能實現的業績。外匯交易蘊含風險。您應該瞭解外匯匯率的波動可能會給您帶來損失。必要或適當時,您應該徵求自己的獨立的財務、稅務或法律顧問的意見或進行此類獨立調查。

本資訊的發佈不是也不構成任何認購或達成任何交易之要約、推薦、邀請或招攬的一部分;在以下情況下,本資訊亦非邀請公眾認購或達成任何交易,也不允許向公眾提出認購或達成任何交易之要約,也不應被如此看待:例如在所在司法轄區或國家/地區,此類要約、推薦、邀請或招攬係未經授權;向目標物件進行此類要約、推薦、邀請或招攬係不合法;進行此類要約、推薦、邀請或招攬係違反法律法規;或在此類司法轄區或國家/地區星展集團需要滿足任何註冊規定。本資訊、資訊中描述或出現的服務或產品不專門用於或專門針對任何特定司法轄區的公眾。

本資訊是星展銀行的財產,受適用的相關智慧財產權法保護。本資訊不允許以任何方式(包括電子、印刷或者現在已知或以後開發的其他媒介)進行複製、傳輸、出售、散佈、出版、廣播、傳閱、修改、傳播或商業開發。

星展集團及其相關的董事、管理人員和/或員工可能對所提及證券擁有部位或其他利益,也可能進行交易,且可能向其中所提及的任何個人或實體提供或尋求提供經紀、投資銀行和其他銀行或金融服務。

在法律允許的最大範圍內,星展集團不對因任何依賴和/或使用本資訊(包括任何錯誤、遺漏或錯誤陳述、疏忽或其他問題)或進一步溝通產生的任何種類的任何損失或損害(包括直接、特殊、間接、後果性、附帶或利潤損失)承擔責任,即使星展集團已被告知存在損失可能性也是如此。

若散佈或使用本資訊違反任何司法轄區或國家/地區的法律或法規,則本資訊不得為任何人或實體在該司法轄區或國家/地區散佈或使用。本資訊由 (a) 星展銀行集團公司在新加坡;(b) 星展銀行(中國)有限公司在中國大陸;(c) 星展銀行(香港)有限責任公司在中國香港[DBS CY1] ;(d) 星展(台灣)商業銀行股份有限公司在台灣;(e) PT DBS Indonesia 在印尼;以及 (f) DBS Bank Ltd, Mumbai Branch 在印度散佈。

相關見解

- 人民幣雙向波動27 Aug 2024

- 每周外匯速遞 - 美元續跌 警惕回調風險26 Aug 2024

- Economics Weekly: Continued Moderation16 Aug 2024

相關見解

- 人民幣雙向波動27 Aug 2024

- 每周外匯速遞 - 美元續跌 警惕回調風險26 Aug 2024

- Economics Weekly: Continued Moderation16 Aug 2024