- Equities: Global equities declined as the market rotated away from tech giants and toward value and small-cap stocks

- Credit: Credit investors have a unique opportunity to lock in high yields and benefit from price gains as the market anticipates Fed easing and a steepening yield curve

- FX: DXY’s outlook becoming less predictable given low visibility on Fed’s policy timing and Trump Trade; possibility of MAS slightly easing the slope of SGD NEER policy band

- Rates: Caution needed as USTs sell off with stocks; more market volatility appears inevitable as US elections draw near

- The Week Ahead: Keep a lookout for US Change in Initial Jobless Claims; Singapore Inflation

相關見解

- 套利交易拆倉潮高峰或已過去13 Aug 2024

- 每周外匯速遞 - 套息拆倉告一段落 關注美國CPI13 Aug 2024

- Multi-Asset Weekly: US Equities Dip Amid Volatile Market Conditions12 Aug 2024

Volatility and uncertainty drive global equity weekly declines. In the US market, there has been a notable shift in market dynamics for the week, characterized by a pronounced rotation out of technology megacaps and into cyclical and small-cap stocks. This led to the S&P 500's largest weekly drop since April, with the index shedding around 2%. The tech-heavy Nasdaq 100 bore the brunt of the sell-off, plummeting nearly 4% while the Russell 2000 small-cap index outperformed, gaining 1.7% for the week. This divergence underscores the market's evolving sentiment and the potential for a broadening rally beyond the leadership of megacap tech stocks.

Adding to the volatility were concerns over a global cyber outage that disrupted multiple industries. The Europe Stoxx 600 Tech Index ended the week 2.7% lower, and Japan's Nikkei 225 fell 2.7% due to concerns over tighter US restrictions on semiconductor exports to China. During China's third plenum, the Hang Seng Index retreated 0.5% for the week due to a lack of clarity on the execution of initiatives, alongside a concerning downside surprise in 2Q GDP.

Topic in focus: Japan equities – Benefits and challenges of a weak yen. The yen's depreciation to a 38-year low against the dollar has made Japan an attractive destination for overseas travellers. The tourism industry is expected to become Japan's second-largest export sector in 2024, trailing only the automotive industry and surpassing electronic components. While a weaker yen boosts export revenues, corporate profits, and wage growth, several issues persist.

Export volumes remain stagnant and real wages are declining. Additionally, the weaker yen accelerates imported inflation, complicating the Bank of Japan's efforts to normalise monetary policy. Both core and wholesale inflation had risen in June, keeping alive market expectations of a near-term interest rate hike, while both business and consumer sentiments remain weak. The country is also facing an “overtourism” crisis with crowded trails and excessive littering at popular tourist spots. It also puts pressure on Prime Minister Kishida’s government, as declining purchasing power weakens domestic sentiment. The Japanese government has reduced its growth forecast for this year to 0.9% as rising import costs – arising from the weak yen – have impacted consumption, highlighting the patchy nature of Japan’s economic recovery.

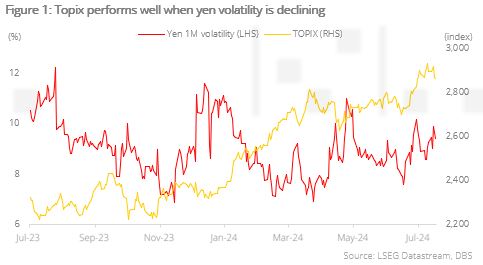

Yen volatility, driven by extensive carry trades and intervention risks, has unsettled Japan’s equity markets. Previously fuelled by "Kishidanomics," the market is likely to pause and shift towards themes that generate alpha, such as AI beneficiaries and the financial sector.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

本資訊是由星展銀行集團公司(公司註冊號: 196800306E)(以下簡稱“星展銀行”)發佈僅供參考。其所依據的資訊或意見搜集自據信可靠之來源,但未經星展銀行、其關係企業、關聯公司及聯屬公司(統稱“星展集團”獨立核實,在法律允許的最大範圍內,星展集團針對本資訊的準確性、完整性、時效性或者正確性不作任何聲明或保證(含明示或暗示)。本資訊所含的意見和預期內容可能隨時更改,恕不另行通知。本資訊的發佈和散佈不構成也不意味著星展集團對資訊中出現的任何個人、實體、服務或產品表示任何形式的認可。以往的任何業績、推斷、預測或結果模擬並不必然代表任何投資或證券的未來或可能實現的業績。外匯交易蘊含風險。您應該瞭解外匯匯率的波動可能會給您帶來損失。必要或適當時,您應該徵求自己的獨立的財務、稅務或法律顧問的意見或進行此類獨立調查。

本資訊的發佈不是也不構成任何認購或達成任何交易之要約、推薦、邀請或招攬的一部分;在以下情況下,本資訊亦非邀請公眾認購或達成任何交易,也不允許向公眾提出認購或達成任何交易之要約,也不應被如此看待:例如在所在司法轄區或國家/地區,此類要約、推薦、邀請或招攬係未經授權;向目標物件進行此類要約、推薦、邀請或招攬係不合法;進行此類要約、推薦、邀請或招攬係違反法律法規;或在此類司法轄區或國家/地區星展集團需要滿足任何註冊規定。本資訊、資訊中描述或出現的服務或產品不專門用於或專門針對任何特定司法轄區的公眾。

本資訊是星展銀行的財產,受適用的相關智慧財產權法保護。本資訊不允許以任何方式(包括電子、印刷或者現在已知或以後開發的其他媒介)進行複製、傳輸、出售、散佈、出版、廣播、傳閱、修改、傳播或商業開發。

星展集團及其相關的董事、管理人員和/或員工可能對所提及證券擁有部位或其他利益,也可能進行交易,且可能向其中所提及的任何個人或實體提供或尋求提供經紀、投資銀行和其他銀行或金融服務。

在法律允許的最大範圍內,星展集團不對因任何依賴和/或使用本資訊(包括任何錯誤、遺漏或錯誤陳述、疏忽或其他問題)或進一步溝通產生的任何種類的任何損失或損害(包括直接、特殊、間接、後果性、附帶或利潤損失)承擔責任,即使星展集團已被告知存在損失可能性也是如此。

若散佈或使用本資訊違反任何司法轄區或國家/地區的法律或法規,則本資訊不得為任何人或實體在該司法轄區或國家/地區散佈或使用。本資訊由 (a) 星展銀行集團公司在新加坡;(b) 星展銀行(中國)有限公司在中國大陸;(c) 星展銀行(香港)有限責任公司在中國香港[DBS CY1] ;(d) 星展(台灣)商業銀行股份有限公司在台灣;(e) PT DBS Indonesia 在印尼;以及 (f) DBS Bank Ltd, Mumbai Branch 在印度散佈。

相關見解

- 套利交易拆倉潮高峰或已過去13 Aug 2024

- 每周外匯速遞 - 套息拆倉告一段落 關注美國CPI13 Aug 2024

- Multi-Asset Weekly: US Equities Dip Amid Volatile Market Conditions12 Aug 2024

相關見解

- 套利交易拆倉潮高峰或已過去13 Aug 2024

- 每周外匯速遞 - 套息拆倉告一段落 關注美國CPI13 Aug 2024

- Multi-Asset Weekly: US Equities Dip Amid Volatile Market Conditions12 Aug 2024