Related insights

Today’s US monthly jobs report will be important to the USD. The strong US labour market is why markets think the Fed believes the neutral rate is near. Interest rate futures see the Fed delaying rate cuts to June and October, a factor that kept the USD strong. Nonfarm payrolls are anticipated to slow to 175k in January after the better-than-expected increase to 256k in December. However, we cannot rule out surprises. ADP Employment increased to 183k in January, more than the 150k consensus, while December was revised to 176k from 122k. The ISM Services employment index rose to 52.3 from 51.3 while the 4-week moving average initial jobless claims eased to 217k from 223k. Pay attention to the University of Michigan’s consumer survey, which showed that one-year inflation expectations have increased to 3.3% in January from 2.8% in December. Next week, US CPI and core inflation are expected to remain sticky at 0.3% MoM in January.

Fed Chair Jerome Powell will present his semi-annual congressional testimonies on monetary policy next week. Powell should reinforce the Fed’s cautious approach to lowering rates this year, telling US lawmakers that more clarity will be needed on Trump’s policies on tariffs, tax cuts, and immigration before the next move. With the Fed cautious and Trump delaying tariffs on Canada and Mexico by a month, markets have been looking at shorting yen crosses again. TheBank of Japan has flagged more hikes this year, while other central banks lowered rates to cushion their economies from potential US tariffs that heighten global trade tensions. For example, AUD/JPY is eyeing last August’s low of 93.7 after breaking below its two-month support at 96. The futures market is pricing a 96% chance of the Reserve Bank of Australia joining the global easing cycle on February 18.

There were essential takeaways from US Treasury Secretary Scott Bessent’s interview on Bloomberg TV. First, Bessent would refrain from criticizing Powell, trusting him to make the right decisions on monetary policy. He was more concerned about the US Treasury 10Y yield, which influences the mortgage market, than the Fed Funds Rate. Second, Bessent expected the strong USD policy to be completely intact under Trump but did not want other countries to manipulate their currencies for unfair trade advantages. Third, Bessent warned that China would end up “eating quite a bit of tariffs”, adding that China was the most unbalanced economy in the history of the world.

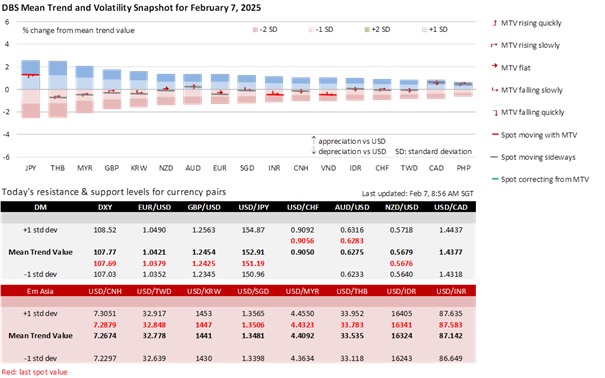

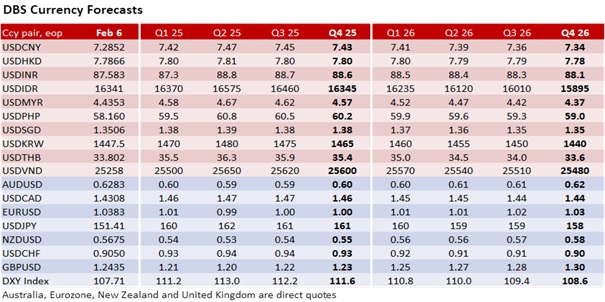

GBP/USD failed to trade above 1.25 again this year, in line with our expectations. The Bank of England’s decision to lower the bank rate by 25 bps to 4.50% was dovish. Two Monetary Policy Committee members – Catherine Mann (the hawk) and Swati Dhingra (the dove) – wanted a larger 50 bps cut. Apart from the bank rate matching the upper bound of the Fed Funds Rate, the BOE also adopted a “careful” approach to rates, mirroring the Fed’s “cautious” stance. The BOE looked past its own expectation for CPI inflation to rise from 2.5% YoY in December to 3.7% in 1H25, driven temporarily by higher energy prices and increases in some regulated prices. The MPC reckoned weak demand and a negative output gap would eventually return inflation to the 2% target. Bank staff expected the UK economy to contract by 0.1% QoQ saar in 4Q24, in contrast to the 0.3% growth projected in the November report. The subsequent recovery in 1Q25 is now seen weaker at 0.4% instead of 1.4% amid a higher unemployment rate of 4.5% vs. 4.1% previously. The forecasts did not factor in US tariffs, which the BOE considered a threat to the UK’s growth by encouraging businesses to delay investments and consumers to increase savings. The stagflation outlook should keep the market alert to fiscal slippage risks in Chancellor Rachel Reeve’s budget. The Office for Budget Responsibility (OBR) will likely downgrade its 2% growth forecast for 2025 in the March Spring Budget Statement. We maintain our forecast for GBP/USD to fall to 1.20 by mid-2025.

Quote of the Day

“The people of this country want an industrial policy that is for America and Americans.”

US President William McKinley

February 7 in history

The Maastricht Treaty was signed in 1992, leading to the creation of the European Union.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.