- Momentum in Europe has faded amid a weak growth outlook and suppressed equity valuations.

- Opportunities remain in the IT services and healthcare sectors, as well as select luxury players.

- Growth in the financial sector has been subdued, with net interest margins likely to be compressed by further rate cuts.

- Rate cuts and easing energy prices boost the utilities sector.

Related insights

- ECB Eases Amid Disinflation25 Oct 2024

- Mapletree Industrial Trust25 Oct 2024

- Singapore Equity Picks25 Oct 2024

Coming up short. Europe began the year on a positive note amid a pickup in growth and sentiment, sparking optimism that the region’s economic difficulties might be receding. Promising signs of recovery had led to a hopeful outlook for the remainder of the year, but as the year progressed, momentum in European equities largely dissipated.

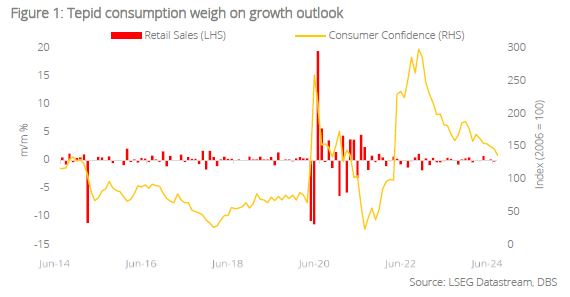

Eurozone GDP expanded 0.3% q/q in 2Q, the same pace as the quarter before, suggesting that the economy is recovering from last year’s stagnation. However, soft manufacturing and industrial production numbers continue to dim the growth outlook; despite earlier signs of improvement, the German economy fell back into contraction in the second quarter after recording a 0.1% decline in GDP, disappointing expectations of an upward revision.

Events in recent months saw heightened volatility in Europe markets. Europe stocks, though cheap, were not spared from the recent market rout triggered by weak US labour market data and a sharp unwinding of the yen carry trade; earlier on, French President Emmanual Macron’s abrupt call for snap elections had sent French stocks and bonds into a sharp selloff, triggering concerns of contagion risks. These risk-off events will dent investors’ appetite for European stocks in the short term.

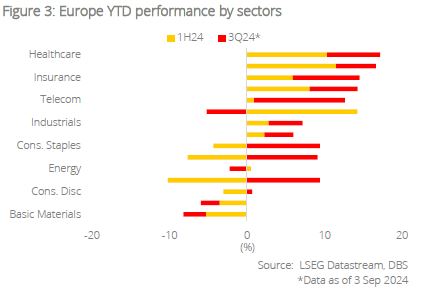

No imminent rebound in sight. Despite already trading at steep discounts to US stocks, the unremarkable earnings season has failed to lift valuations. Of the 76% of companies which have reported their earnings (as of 26 Aug), only 54% have registered positive earnings surprises, mainly in the communications, financials, and real estate sectors. Growth in the financial sector has been subdued, with net interest margins likely to be compressed by further rate cuts. Meanwhile, the pullback in spending on autos and luxury goods continue to weigh on the consumer discretionary sector.

Stay with resilient sectors. In the near-term, weak sentiment will further compress equity valuations, which are already near historic lows. Until we see a significant decline in bond yields or a substantial improvement in corporate earnings, the sustainability of gains in Europe equities remains doubtful. We maintain our underweight position on Europe equities, and highlight fundamentally driven sector-specific opportunities in the IT services and healthcare sectors, as well as select luxury players. We are optimistic on the utilities sector, which is likely to benefit from lower input costs as rates and oil prices decline, as well as an uptick in demand from AI-driven energy needs.

With healthcare playing a major role in Europe’s stock market, we remain cognisant of key risks facing the sector. Drugs such as Ozempic have been around for years, but have only made headlines recently due to their overnight popularity as weight loss agents.

Such drugs mimic a hormone (GLP-1) in the body that helps to control insulin and blood glucose levels, making them viable for diabetes treatment. A recent study by the American Journal of Medical Care found that nearly 40% of patients with type 2 diabetes discontinued their insulin medication within 12 months of it being prescribed – researchers noted that the results were particularly pronounced with people who started taking GLP-1 drugs. Companies must constantly innovate to stay ahead of the curve, or risk becoming obsolete.

That said, the healthcare sector remains subjected to strict regulatory controls. New EU rules announced this year have threatened to cut the number of new treatments for rare diseases because of stricter curbs on medical trials, potentially reducing treatment options for rare diseases. These rules may stifle investments into medical breakthroughs, as some pharma companies may be left with no choice but to abandon their research on rarer diseases.

Stay with quiet luxury. The global luxury sector is facing a period of uncertainty, as consumer confidence wanes over subdued economic growth and persistent inflation. McKinsey forecasts the sector to grow by 3–5% in 2024, down from 5–7% in 2023, as luxury spending continues to be weighed down by key growth drivers such as China. A 2024 survey by PwC suggests that shoppers are shunning luxury items in favour of essentials; about 40% of respondents anticipate that they will be spending less or nothing at all on luxury goods over the next six months.

Still, we believe pockets of growth exist. Markets such as Japan are emerging as new growth areas – Savills’ Global Luxury Retail 2024 Outlook shows that while new store openings fell 12% in China, the wider Asia Pacific region reported an increase in new store activity. Tokyo and Singapore were key behind this increase, helped by a pick-up in tourism and a weak yen, in the case of Japan. We maintain our view that luxury is a long-term structural growth sector; in particular, widening income gaps will highlight less price-sensitive and more exclusive, experiential driven demand. As the industry continues to be challenged by near-term headwinds, stay with quiet luxury brands that adapt to changing preferences and offer more than just material satisfaction, making them more resilient to economic downturns.

Renewables present fresh opportunities. Post the dual shocks of the pandemic and the Russia Ukraine war, European governments were alarmed by the region’s reliance on foreign supply of energy and fossil fuels. The ensuing energy crisis shored up the urgency in transitioning Europe to green energy – the EU has set a target to reduce net greenhouse gas emissions by at least 55% by 2030; alongside policies focused on increased deployment of renewables and energy efficiency, there is also a focus on the diversity and resilience of clean energy supply chains, both for manufacturing and for critical minerals.

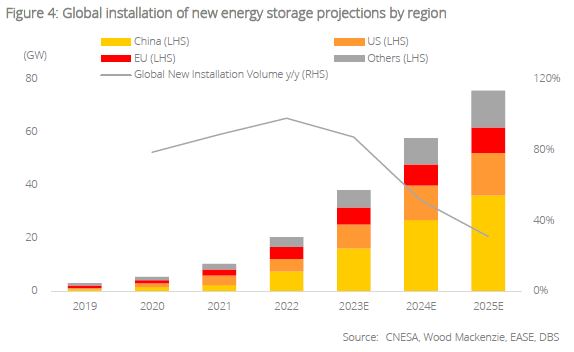

In 2023, investment in renewables generation totalled almost USD110bn, an increase of more than 6% from the previous year, according to the International Energy Agency. Denmark and Germany remain at the forefront of the wind power sector in Europe despite ongoing profitability challenges, while Spain has led the surge in solar adoption to see wholesale electricity prices fall to record lows during periods of high solar output. A shift to cleaner and more secure energy sources is set to create significant opportunities to invest in renewable energy generation, grid networks for distribution, energy storage solutions, and new mobility.

Opportunities in infrastructure development. The need for infrastructure development is intensifying worldwide, fuelled by the aging of existing assets and the rapid expansion of opportunities across traditional and emerging sectors. Roads and bridges aside, modern infrastructure includes advanced assets such as EV charging stations, data centres, smart grids, and more. To tackle the concurrent challenges of climate change and deteriorating infrastructure, global infrastructure upgrades are crucial for enabling disruptive technologies and improvements in manufacturing capacities.

As global politics become more fragmented, nations are focusing on energy security, supply chain resilience, and increasing domestic manufacturing, leading to new infrastructure projects. Developed markets, especially those in Europe, grapple with ageing infrastructure. The EU’s power grid, for example, averages 40 years old. To this end, the EU is investing heavily in infrastructure, including over EUR7bn in grants for transport projects, primarily railways. Additionally, the EU is contemplating a EUR100bn fund to boost defence manufacturing.

European companies poised to benefit from this long-term trend include those that specialise in: 1) engineering and construction services, 2) production of raw materials and composites used in infrastructure development, 3) manufacturing and distribution of heavy construction equipment and products, 4) infrastructure transportation, and 5) the production or sale of smart grid components.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- ECB Eases Amid Disinflation25 Oct 2024

- Mapletree Industrial Trust25 Oct 2024

- Singapore Equity Picks25 Oct 2024

Related insights

- ECB Eases Amid Disinflation25 Oct 2024

- Mapletree Industrial Trust25 Oct 2024

- Singapore Equity Picks25 Oct 2024