Related insights

- Vertex Pharmaceuticals28 Oct 2024

- Moderna Inc 28 Oct 2024

- International Business Machines Corp28 Oct 2024

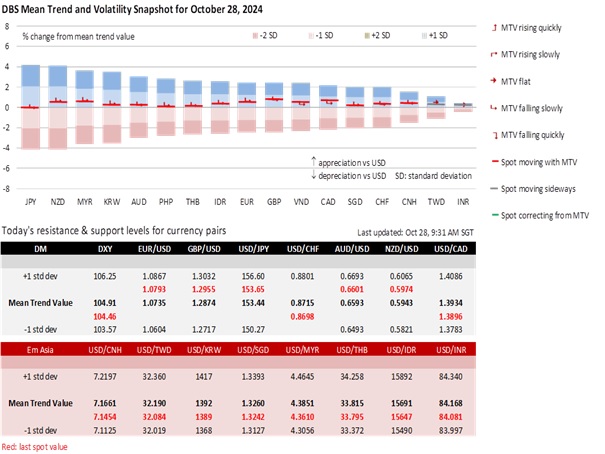

We remain cautious of the greenback’s recovery after the DXY Index’s 3.9% rise in the past four weeks. With the Fed in a pre-FOMC blackout, weaker US nonfarm payrolls this Friday could reinvigorate expectations for two Fed cuts in November and December. US initial jobless claims have risen on a 4-week moving average basis to 239k for the week ending October 18, the highest since early August. Consequently, nonfarm payrolls may fall below 200k, reversing September’s unexpected rise to 223k, which triggered the USD’s recovery and the rise in US bond yields this month.

The “Trump Trade” that lifted the USD could lose momentum ahead of the US Presidential Election on November 5, mirroring a similar loss 1-2 weeks before the 2016 election. The race between Vice President Kamala Harris and former President Donald Trump remains too close to call. However, according to NBC News, early votes showed Harris leading in Pennsylvania, Michigan, and Wisconsin – the three critical swings states in the 2016 and 2020 elections. Additionally, the DXY’s post-election rally in 2016 was also fuelled by the onset of a Fed hiking cycle in December 2016, a stark contrast to today’s scenario, where the Fed began a rate-cutting cycle last month.

The JPY started weak on Monday amid post-election uncertainties and doubts over BOJ policy. Prime Minister Shigeru Ishiba, who triggered this month’s JPY sell-off with his comment about Japan’s unreadiness for rate hikes, will have difficulty hanging on to power. Exit polls indicated that the ruling coalition led by the Liberal Democratic Party (LDP) would lose its parliamentary majority in the October 27 snap elections. Ishida, who has 30 days to find a third coalition partner, will likely face pressure to resign. JPY bears hope that Sanae Takaichi, a strong advocate of ultra-low interest rates, will succeed him. Meanwhile, the opposition Constitutional Democratic Party will also be looking to form another coalition to form a government.

The Bank of Japan is expected to leave rates unchanged at its meeting on October 31, following the decline in Tokyo’s CPI inflation below the 2% target in October. But it should maintain its monetary policy normalization plan to hike rates through 2025. The largest labor union group, Rengo, has announced plans to seek wage hikes of at least 5% in 2025, matching this year's increase. Markets will view interventions as opportunities to buy USD/JPY but they should also be wary of the USD’s downside risks on a weaker US payrolls report this Friday.

GBP/USD traded below 1.30 last week but found support at a trendline of around 1.29. The UK Autumn Budget 2024 announcement on October 30 has attracted attention. Chancellor of the Exchequer Rachel Reeves has flagged some GBP40 bn of tax hikes and spending cuts to plug a GBP22 billion fiscal “black hole” by the previous government. The IMF has given implicit support to relax the self-imposed fiscal rule to unleash public investment, namely in infrastructure, to achieve long-term growth. Hence, the market does not expect a repeat of the mini-budget crisis, especially now that CPI inflation fell to 1.7% YoY in September, below the 2% target for the first time since April 2021. The OIS market has priced a 25 bps cut in the Bank of England’s bank rate to 4.75% at its next meeting on November 7.

Quote of the Day

“If the freedom of speech is taken away, then dumb and silent we may be led, like sheep to the slaughter.”

George Washington

October 28 in history

The Statue of Liberty was officially inaugurated in 1886.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Vertex Pharmaceuticals28 Oct 2024

- Moderna Inc 28 Oct 2024

- International Business Machines Corp28 Oct 2024

Related insights

- Vertex Pharmaceuticals28 Oct 2024

- Moderna Inc 28 Oct 2024

- International Business Machines Corp28 Oct 2024