Related insights

- India rates: 2H Fiscal year borrowing calendar in view 27 Sep 2024

- Mixed markets with a weakish USD tone27 Sep 2024

- RMB strength and CHF watched ahead of SNB 26 Sep 2024

China's key policymakers held a Politburo meeting on Thursday to chart an urgent course correction for the economy. In a notable shift in tone and substance, the Politburo vowed forceful action across several critical fronts to stabilize key sectors and restore growth momentum. The unscheduled September meeting, atypical of the usual April, July, and December sessions, highlighted the urgency policymakers faced. The language in the statement also marked a contrast. Specifically, removing terms like "prudent" in describing monetary policy and pledging a "forceful" implementation of rate cuts, signals the urgency policymakers felt to tackle the economic slowdown.

In their strongest housing pledge to date, officials committed to halting the decline in the property market, which saw new home prices decline at the fastest pace in nine years in August. Construction of new housing projects would also face stricter curbs to alleviate oversupply, while 'whitelist' loans for unfinished developments would be scaled up. To drive much-needed investment, local governments were urged to accelerate the issuance and deployment of special bonds towards infrastructure. Seen as the most direct means to spur near-term demand, local spending has faced hurdles in project selection amid deleveraging efforts.

On asset markets, the commitment to "boost the equity market" was notably more encouraging than previous vows simply to "improve stability." The language implies leaders aimed to buoy confidence through rising share prices. The Politburo further pledged stronger support for job seekers and lower-income groups, building on recent cash aid for those facing hardship. Boosting employment could help the ailing retail sector, where sales growth in August hovered among the slowest paces in years.

While details on fiscal spending increases were not provided, RMB2 trn in special sovereign bonds were reportedly planned for the year. This issuance would complement recent monetary easing by the PBOC, seeking to restore confidence through accelerated fiscal efforts amid weak private sector credit demand.

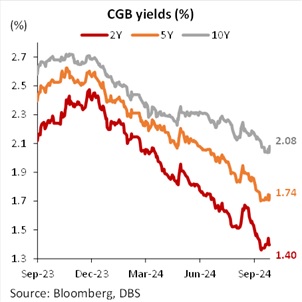

In our view, bear steepening of the CGB curve will likely play out in the near-term. The short-end 2Y yield will stay anchored amid the 30bps 1Y MLF rate cut announced earlier this week. Meanwhile, the long-end 10Y yield will see further upward pressure due to the special sovereign bond issuance. The return of investor confidence in the Chinese economy will also contribute to the upward march.

Topic

Explore more

E & S Macro StrategyGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- India rates: 2H Fiscal year borrowing calendar in view 27 Sep 2024

- Mixed markets with a weakish USD tone27 Sep 2024

- RMB strength and CHF watched ahead of SNB 26 Sep 2024

Related insights

- India rates: 2H Fiscal year borrowing calendar in view 27 Sep 2024

- Mixed markets with a weakish USD tone27 Sep 2024

- RMB strength and CHF watched ahead of SNB 26 Sep 2024