- Equities: Global equities rebound strongly after early Aug sell-off, driven by positive economic data and rate cut optimum

- Credit: As rate tightening cycle nears its end, investors can clip the higher coupons in IG credit on lower volatility as rates and spreads are no longer highly correlated

- FX: USD/JPY eyeing lower levels after its short covering from 141.70 on 5 Aug; USD/THB has the scope to fall further to 34 on a weaker USD

- Rates: Panic in USD rates receded; no longer makes sense for the market to factor in aggressive Fed easing

- The Week Ahead: Keep a lookout for US Change in Initial Jobless Claims; Japan CPI

Related insights

- Cloudy Outlook Ahead30 Aug 2024

- FX Tactical Ideas: Long AUD-NZD at Bottom of Ascending Channel30 Aug 2024

- CDL Hospitality Trusts30 Aug 2024

Stocks continue recovery amid optimism. Following the early August sell-off, stocks rebounded strongly with Nasdaq leading the recovery, up 5.3% for the week, followed by the S&P 500, up 3.9%. This was supported by positive retail sales and cooling inflation data, its lowest reading in more than three years. However, the housing sector showed signs of strain with building permits and housing starts dropping to their lowest levels since the early pandemic.

European markets rallied alongside the US, buoyed by expansion of the Eurozone economy, +0.3% in 2Q. The Euro STOXX 50 and Dax were up 3.5% and 3.4% for the week. Over in Japan, the Nikkei 225 was up 8.7%, supported by a weaker yen and stronger than expected US economic data. China, on the other hand, saw modest gains despite posting weaker-than-expected industrial production numbers and continued declines in new home prices. The SHCOMP and Hang Seng were up 0.6% and 2.0% for the week.

Topic in focus: Tactical play on small caps as Fed policy eases. On Wednesday (14 Aug 2024), July’s CPI numbers came in lower than expected (2.9% y/y vs consensus 3.0% y/y), and it marks the first time since Mar 2021 that CPI has fallen below 3%. This strengthens the case for initiating a rate cut cycle in September which will likely benefit small caps. Medium-term momentum for the small caps space include:

- Rate cuts and lower borrowing cost to buoy small caps earnings: Small caps companies have a larger proportion of debt maturing within five years as compared to larger companies (c.67% for S&P 600 Small Cap vs c.45% for S&P 500). As the Fed embarks on monetary easing, small cap companies will be able to refinance at lower rates, reduce their borrowing cost, and boost earnings.

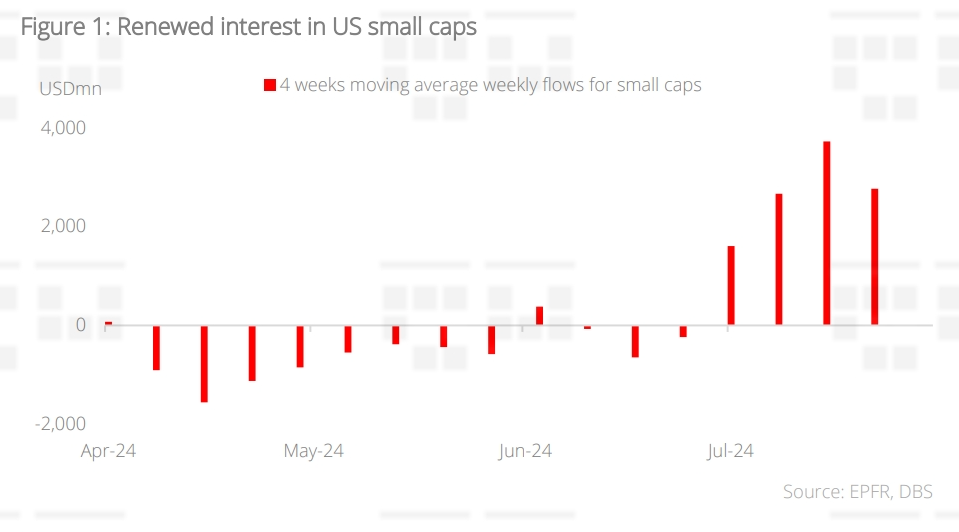

- Fund flows suggest renewed interest in US small caps as rate cuts loom: In the three months before June's CPI data release, small cap equity funds saw weekly outflows. Since the release of June’s data (which fuelled expectations of a September cut), small cap equity funds attracted a combined inflows of USD11bn in four weeks (ending 7 Aug).

- Attractive “broadening rally” play amid steep valuation discount: At 17.7x, the S&P 600 Small Cap index’s forward P/E is currently well below its 20-year average. Above all, the index is also trading at a 22.9% discount to the S&P 500.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Cloudy Outlook Ahead30 Aug 2024

- FX Tactical Ideas: Long AUD-NZD at Bottom of Ascending Channel30 Aug 2024

- CDL Hospitality Trusts30 Aug 2024

Related insights

- Cloudy Outlook Ahead30 Aug 2024

- FX Tactical Ideas: Long AUD-NZD at Bottom of Ascending Channel30 Aug 2024

- CDL Hospitality Trusts30 Aug 2024