Related insights

- Apple07 Mar 2025

- Salesforce Inc07 Mar 2025

- FX Tactical Ideas | Risk-off and EUR-centric Dynamics Lead the Market07 Mar 2025

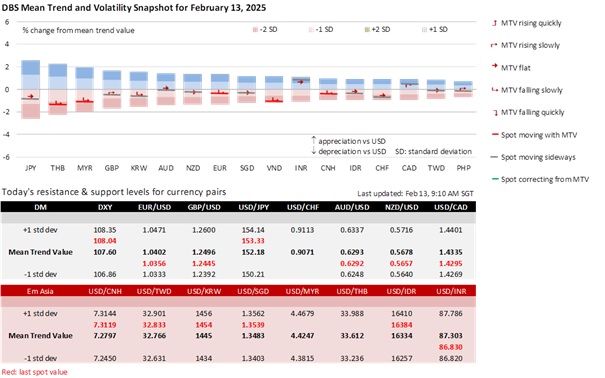

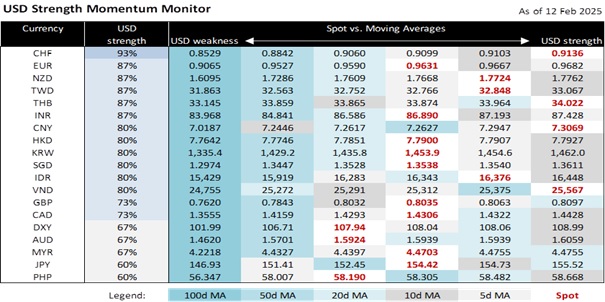

The DXY Index initially surged to 108.52 on higher-than-expected US CPI inflation. Headline inflation increased by 0.5% MoM in January instead of slowing to 0.3% consensus from 0.4% in December. Excluding food and energy prices, core inflation doubled to 0.2% MoM from 0.2%. During his semi-annual testimony to the House Financial Committee, Fed Chair Jerome Powell said the Fed would respond to the higher inflation print by keeping monetary policy restrictive for now.

Powell added that today’s PPI data would shed some light on PCE inflation. Like CPI, consensus also expects PPI and core inflation to be sticky at 0.3% MoM in January. Powell said the dot plot was not a forward guidance, which may fuel expectations for the Fed to reduce further this year’s rate cut projections in the upcoming March Summary of Economic Projections. After the Fed’s third rate cut in December, the Fed reduced its projections to two cuts from four cuts. The US Treasury 10Y yield rose overnight by 8.6 bps to 4.62%, its highest level since January 24. The futures market is pricing in only one cut in July this year.

However, the DXY plunged to 107.63 in hopes of an early end to the Russia-Ukraine war following a surprise phone call between US President Donald Trump and Russian President Vladimir Putin. The news sent the EUR/USD, which initially fell to 1.0317 on the stronger-than-expected US CPI print, higher to 1.0430. However, as reality sets in, EUR/USD returned below 1.04 to 1.0385. Brussels will likely oppose negotiations without Europe, maintaining that Ukraine’s independence and territorial integrity were non-negotiable. European Commission President Ursula von der Leyen had described Russia’s invasion of Ukraine and Trump’s potential tariffs on the EU with the same word – unlawful. Apart from saddling the EU with a larger defence bill, Trump’s plan could boost far-right movements in the bloc. Germany’s federal elections on February 23 will serve as an early test.

DXY ended the overnight unchanged, near Tuesday’s closing level just below 108. Not everyone believed the higher US CPI inflation was due to seasonal factors. One-year inflation expectations spiked in the University of Michigan’s consumer survey, driven by Trump’s plans on universal tariffs, extension of tax cuts, and mass deportation of illegal migrants. Once again, keep an eye on today’s US PPI data and watch for Ukraine-related volatility.

Quote of the Day

“In politics, stupidity is not a handicap.”

Napoleon Bonaparte

February 13 in history

Tycho Brahe first sketched the “Tychonic system” of the solar system in 1578.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Apple07 Mar 2025

- Salesforce Inc07 Mar 2025

- FX Tactical Ideas | Risk-off and EUR-centric Dynamics Lead the Market07 Mar 2025

Related insights

- Apple07 Mar 2025

- Salesforce Inc07 Mar 2025

- FX Tactical Ideas | Risk-off and EUR-centric Dynamics Lead the Market07 Mar 2025