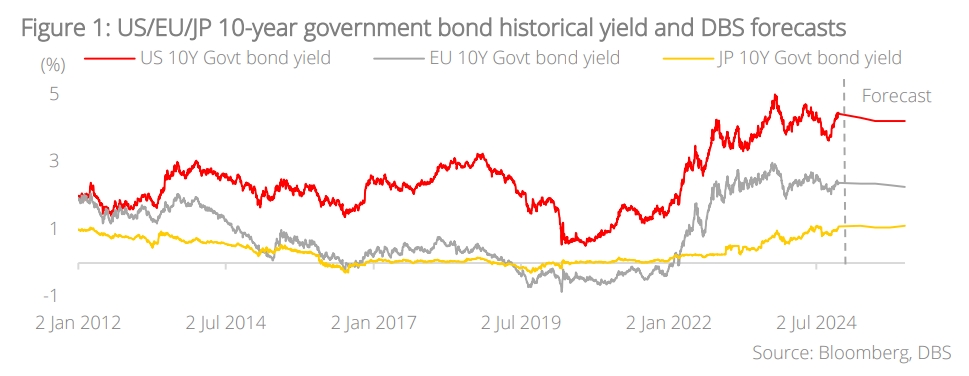

- Rising yields on 10-year government bonds across major markets should support the sale of savings and investment-linked products and continue to enhance recurring investment yields of insurers

- China’s macro economy remains resilient; rolling out of policy stimulus to support market re-rating

- Easing concerns around LGFV and property risks while an improved consumption outlook should support premium growth, benefitting Chinese insurers

- We favour a selective approach and companies with strong underwriting growth and diversified business portfolios; Asia-Pacific regional and China insurers are well-positioned to capitalise on long-term growth opportunities in Asia life insurance market

Related insights

- Global Credit 1Q25 – Making Bonds Great Again23 Dec 2024

- Alternatives 1Q25: Gold – Resilience with Alternatives20 Dec 2024

- CIO Insights 1Q25: Game Changers20 Dec 2024

Trump’s presidency favours life insurers. With Donald Trump’s second term in office, we expect rising interest rates and inflation, driven by his aggressive trade policies and increased pressure on European defence spending. These macroeconomic shifts are likely to have mixed implications for global insurers. For life insurers, a higher-for-longer interest rate environment is expected to provide some tailwinds. Rising yields on 10-year government bonds across major markets should support the sale of savings and investment-linked products and enhance recurring investment yields of insurers. Life insurance claims are less sensitive to inflationary pressures as life policies typically have longer durations and more stable claims patterns. Property and casualty (P&C) insurers are likely to face greater challenges due to claim costs which are more exposed to inflationary pressures. This could pressure underwriting margins, particularly if inflation persists at elevated levels.

Eyeing policy stimulus in China. In China, the potential impact of rising tariffs under a second Trump term may be less severe than previously anticipated. While tariffs may increase pressure on China’s export sector, demand from emerging markets and China’s efforts to reduce its trade deficit could help offset the impact. Moreover, the Chinese government’s ongoing policy stimulus measures are expected to provide substantial support to economic growth and market sentiment. The recent announcement of a RMB6tn debt swap plan, aimed at addressing bad debt in local government financing vehicles (LGFVs), is a key step in stabilising the financial system. Additionally, the planned capital injection into major China banks should facilitate loan book expansion, supporting economic activity across both public and private sectors. Combined with consumption-driven stimulus measures, these actions are likely to result in stable economic growth in China. Insurers in China stand to benefit from a reduction in concerns around LGFV and property risks, while an improved consumption outlook should support premium growth, particularly in the life and health insurance segments.

Selective names with robust growth and diversified business portfolio. We continue to favour Asia-Pacific regional and China insurers which are well-positioned to capitalise on secular growth opportunities in the Asia life insurance market. This sector is expected to outpace global peers in terms of growth, driven by favourable demographics and rising middle-class wealth. Additionally, insurers with strong ties to the high-net-worth (HNW) segment in Asia stand to benefit from an increasing customer base and closer connections across China and ASEAN countries. Any upside surprise in China’s policy stimulus could further catalyse a re-rating of regional and China insurers. We also see attractive opportunities in global insurers with strong market positions and a balanced business mix that can pass rising claim costs to customers and maintain strong premium growth. Companies with significant exposure to Asia—particularly those offering attractive shareholder returns (dividend yield >5%, plus share buyback)—remain our top picks in the global insurance space.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Global Credit 1Q25 – Making Bonds Great Again23 Dec 2024

- Alternatives 1Q25: Gold – Resilience with Alternatives20 Dec 2024

- CIO Insights 1Q25: Game Changers20 Dec 2024

Related insights

- Global Credit 1Q25 – Making Bonds Great Again23 Dec 2024

- Alternatives 1Q25: Gold – Resilience with Alternatives20 Dec 2024

- CIO Insights 1Q25: Game Changers20 Dec 2024